10 THINGS TO KNOW – PRIVATE INSURANCE

Contributing Author: Mark Queen

Faith-based entrepreneurial navigator and founder of Core Score, LLC.

As the principal and CEO of Core Score, I can tell you that the percentage of business leaders who have never heard of reinsurance (private insurance; self insurance) is staggering.

We find it interesting that it took 50 years for the well-known 401k platform to be commonplace in American business; In the spirit of strategic, timely and effective education, Core Score’s representatives are trained and experienced COACHES and NAVIGATORS serving business leaders with strategic business applications including reinsurance. A good reinsurance model is effective, easily adaptable and strategic benefitting qualified candidates. Let’s look at 10 things you should consider if you are exploring this popular platform dating back to the 1600s.

10 Things to Know

1. CHOOSE a PROVIDER which meets the FOUR-WAY TEST

There are many providers in the marketplace, and you should absolutely choose one which is seasoned, compliant, service oriented and communicative. We believe the ‘four-way test’ includes these compliant attributes and critical elements befitting a best-in-class provider:

1) Risk Shifting

Insured contracts with and shifts risk to independent third-party insurer

- Insurer is adequately capitalized, meets tribal statutory requirements

- Meets Tax Court requirements as a bona fide insurance provider

- No caps, indemnification or guarantees by insured

2) Risk Distribution

- Insurer reinsures risk to PORC structure through treaties [reimbursement for claims paid]

- Two reinsurance treaties

- 50% quota share – reinsure insurance company for unrelated risk exposures of the insured

- 50% quota share – pro rata share of all risk retained by Insurer not previously reinsured – unrelated party risk

- Number of insureds

- Number of risk exposures

3) Insurance Risk

Actuarially determined and supported – actual risks of insured that are under insured or uninsured

4) Insurance in the Commonly Accepted Sense

- Properly formed and operated as an insurance company

- Adequately capitalized

- Standard industry policy terms

- Premiums are actuarially supported by independent third-party actuary

- Ensure claims paid

Meets Controlled Group Rules

Ceding fees are a percentage of the premiums paid

2. MANAGE RISK MORE EFFICIENTLY

Traditional insurers cover a large portion of the risks business owners face. However, as many business owners learned during the COVID-19 pandemic, their policies are often limited or exclude coverage. In other words, there are “below the surface” risks inherent to any business operation.

These include uninsured and under-insured risks which large insurers will not cover (or the premium is not cost effective). A solid reinsurance model allows business leaders to mitigate these risks and incorporate best practices into their annual business cycles and long-term planning. See image:

3. UNDERSTAND PREMIUMS are considered TAX-DEFERRED

As you’ve likely realized, remitted premiums are a business expense to any P&L; in other words, while the business owner (insured) is paying premium to address future losses and mitigate business risks, they are also deferring taxes based on the general premise of insurance and statutory accounting. Without a reinsurance plan, business owners are currently self-insuring risks, such as a business interruption, with after-tax money from cash flow.

With a good reinsurance strategy, business leaders augment their P&C policy (often insuring for G&L, workers comp and catastrophic events) with an additional policy giving them expanded coverage, flexibility and control.

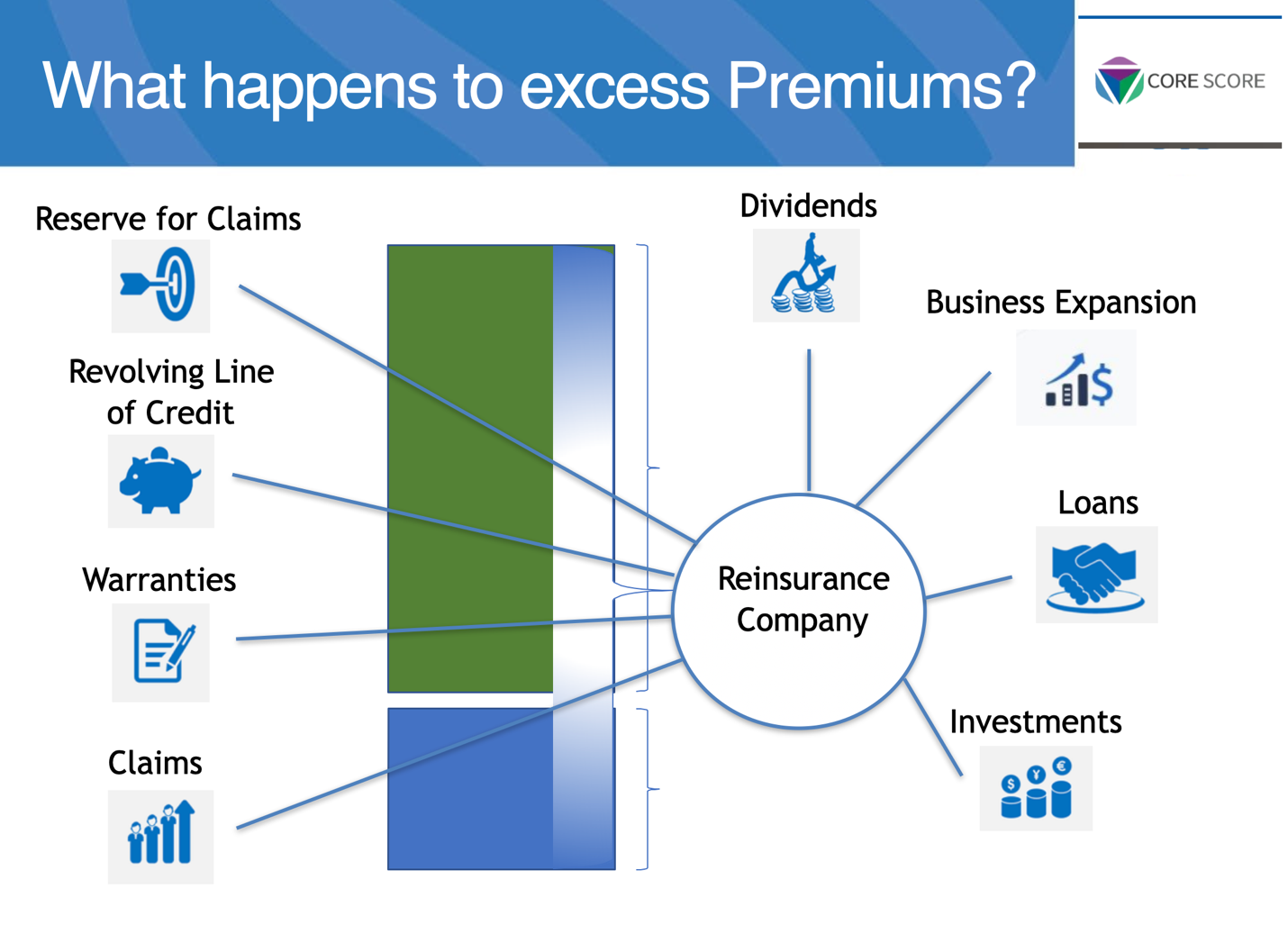

4. YOU’RE IN CONTROL

Once onboarded, business leaders begin to understand the enormous power and flexibility of self-insurance.

The answer to the question ‘What happens to excess premium?’ illuminates the many choices a business leader has.

Beginning with the understanding that premium has enormous asset protection (pending on choice of sovereignty), business leaders are in control of premium assets and have many opportunities which include claims, loans, investments and dividends. See image:

5. DESIGNED TO COMPLIMENT YOUR BUSINESS

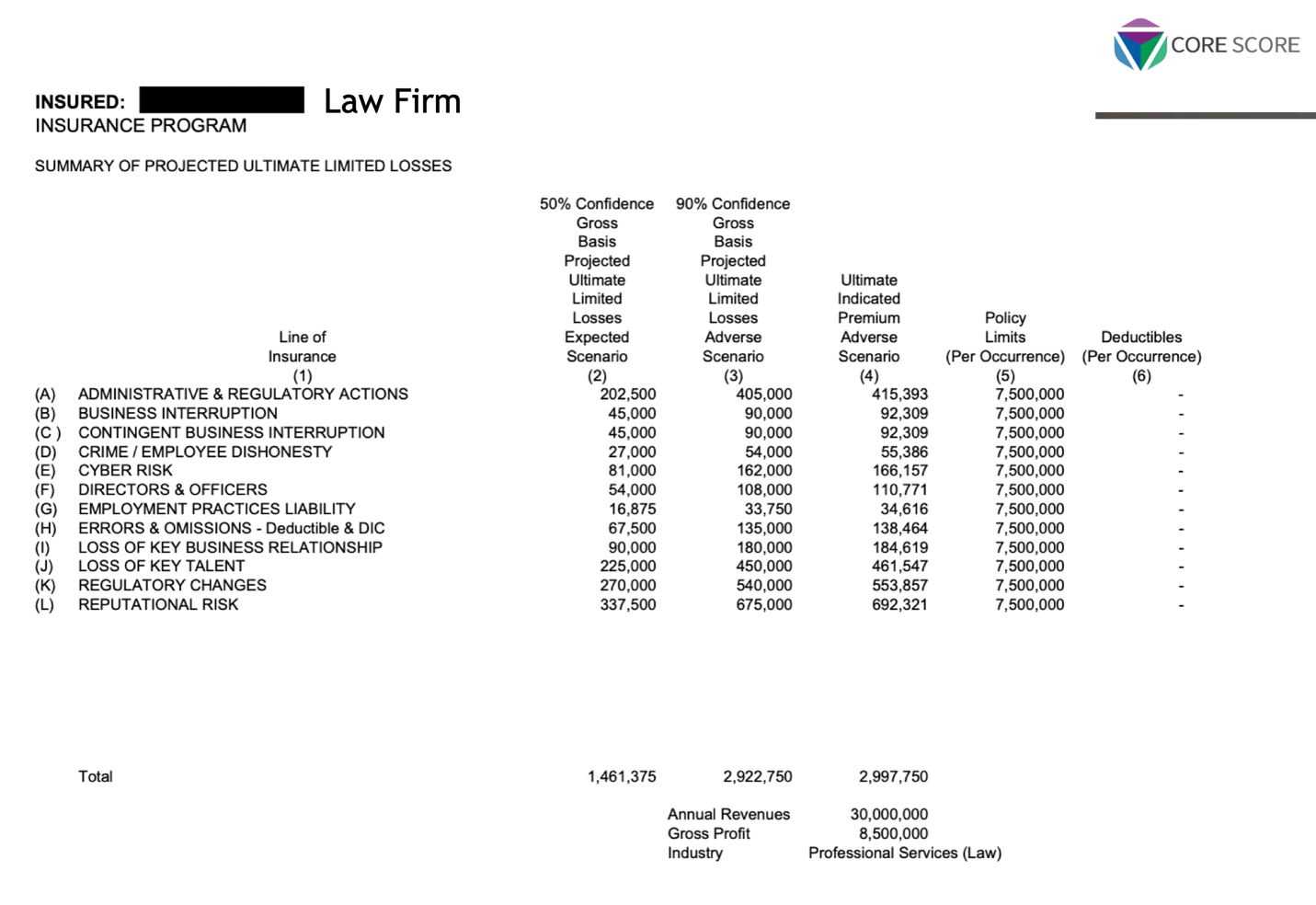

A business leader should choose a plan administrator which passes the four-part test, employs experienced representatives and compliantly helps them achieve risk mitigation, cash flow and asset protection.

After a few years of adopting reinsurance as an alternative risk management tool, executive leaders begin to fully realize the power, flexibility and protection they have in reinsurance; but it starts with choosing a reputable and proven platform (provider, consultant team) which offers onboarding, e-communication, quarterly reviews, compliance checks and ongoing plan maintenance. A seasoned consultant can help you understand details of the actuarial assessment which determines the terms of the related policy. See summary sample of an actuarial assessment summary page in the LEGAL industry:

6. CONTRIBUTION LIMITS

Core Score recommends a platform which does not use the 831(b) election. 831(b) election is often associated with the history of IRS scrutiny and has annual contribution limits. 831(b) is most often associated with the word ‘captive’ or ‘micro captive’ and is often a state-based structure.

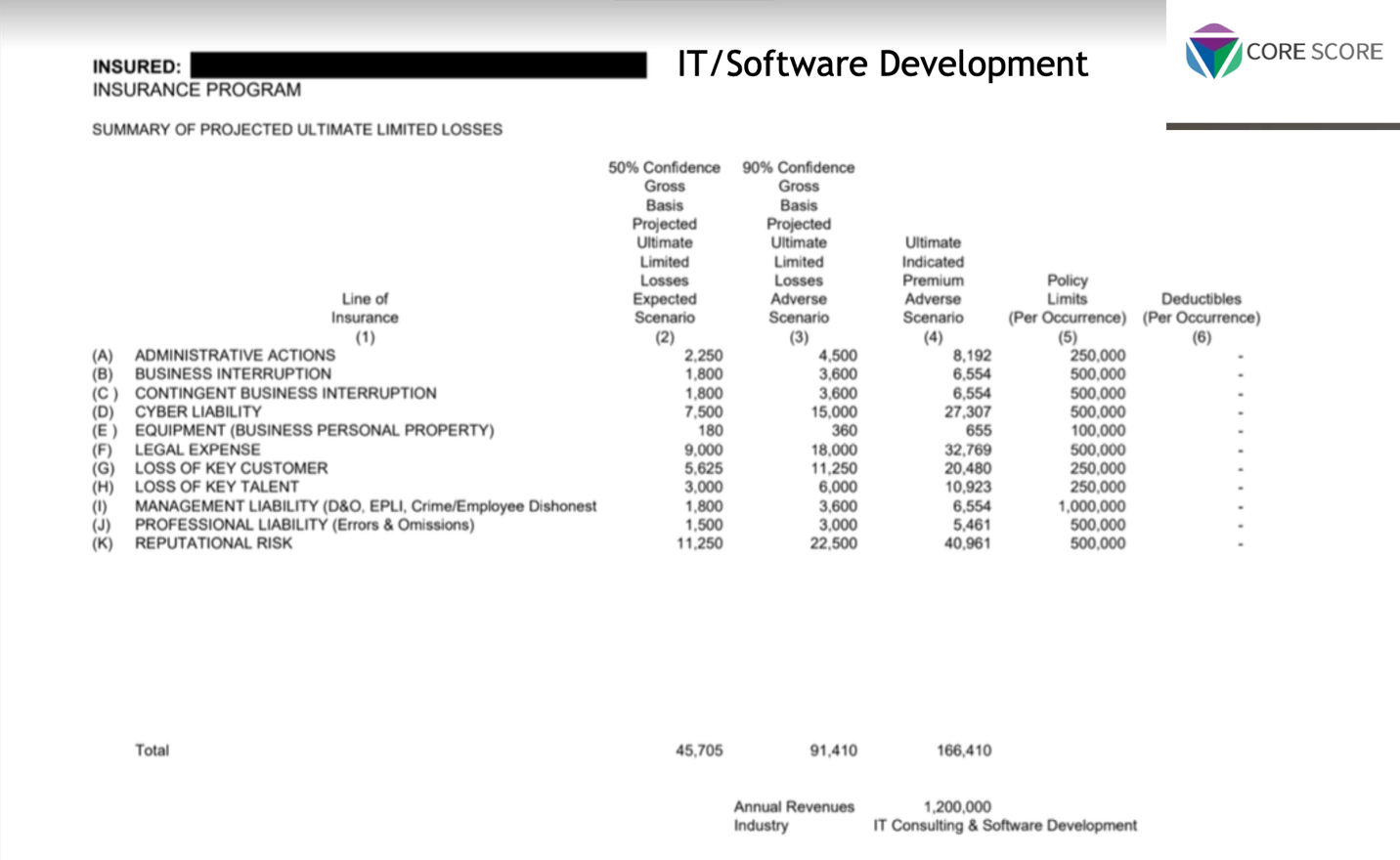

Alternatively, preferable plans exist which operate as a simple linear insurance transaction and use actuarial-based assessments to determine uninsured and under-insured business risks; this data – validated with actuarial science – goes through underwriting and informs the policy issued by the provider (insurance carrier). Core Score recommends a model which a) uses a third-party, licensed actuary; b) uses an actuarial review (risk profile of the business leader) as a basis for the issued policy; c) conducts quarterly or semi-annual reviews (consultative sessions) to determine if relative business risks have increased or decreased risks based on growth or other business dynamics. See summary sample of an actuarial review in the IT/SOFTWARE industry:

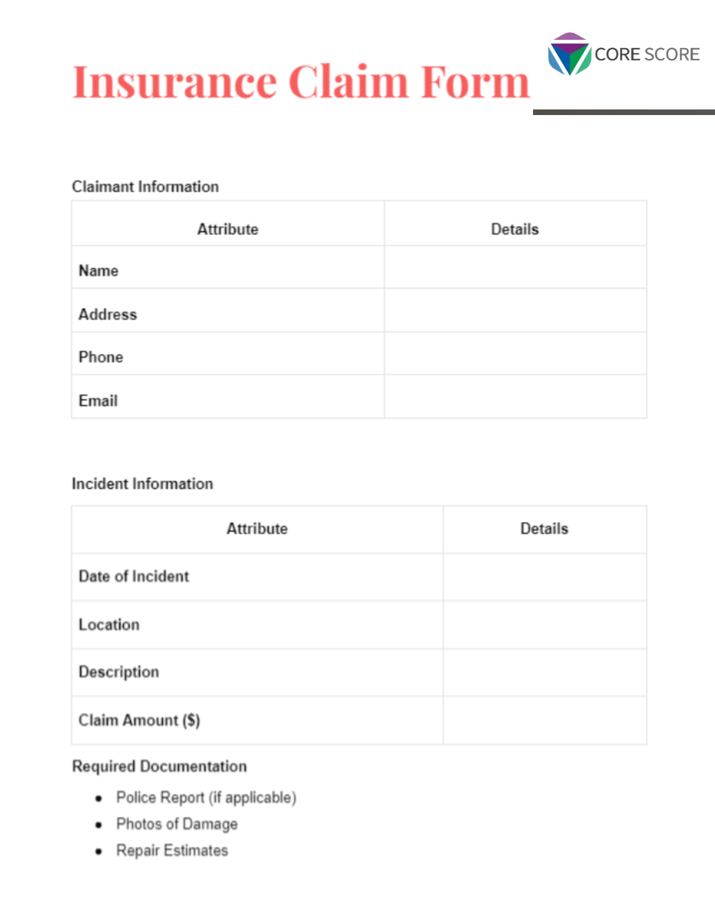

7. CLAIMS are REAL

Private Insurance (e.g., self insurance, reinsurance) is legitimate insurance with global assets totaling $800 billion (Gallagher; 2024).

We know Reinsurance is real (stabilizing insurance company results and enabling growth and innovation to continue) and we also know associated claim management is real. Core Score strongly suggests choosing a model which encourages the filing of claims when warranted.

The good news?

Private Insurance is an exceptional business tool to manage risks which are currently being absorbed by a company’s operations; these line-item risks are real and represent business interruption, legal risks, regulatory risks, reputational risks, loss of key talent, loss of key customer and more.

Choose a provider who supports claim management and is aligned with this compliant insurance element. See simple version of Claims Form:

8. SOVEREINTY MATTERS

It goes without saying that where your reinsurance structure is domiciled is strategic and important.

Typically, the business leader (insured) has three options for domiciling his/her new insurance company; these options represent a) US state; b) offshore; c) tribal (Native American). Each of these options may have its own pros and cons and each are worth exploring in your due diligence.

We find that using a Native American tribe for domiciling a business leader’s insurance structure (i.e., using the tribe’s legal jurisdiction/sovereignty dating back to 1934) has the advantages of an offshore account while still avoiding a US state’s heavy restrictions, over regulation and exorbitant costs. Importantly, domiciling the insurance company with a Native American tribe is classified as DOMESTIC; meaning, the new insurance company is not formed offshore account requiring the 953(d) election. The term “953(d) election” refers to a decision made by a foreign insurance company to be taxed as a United States taxpayer.

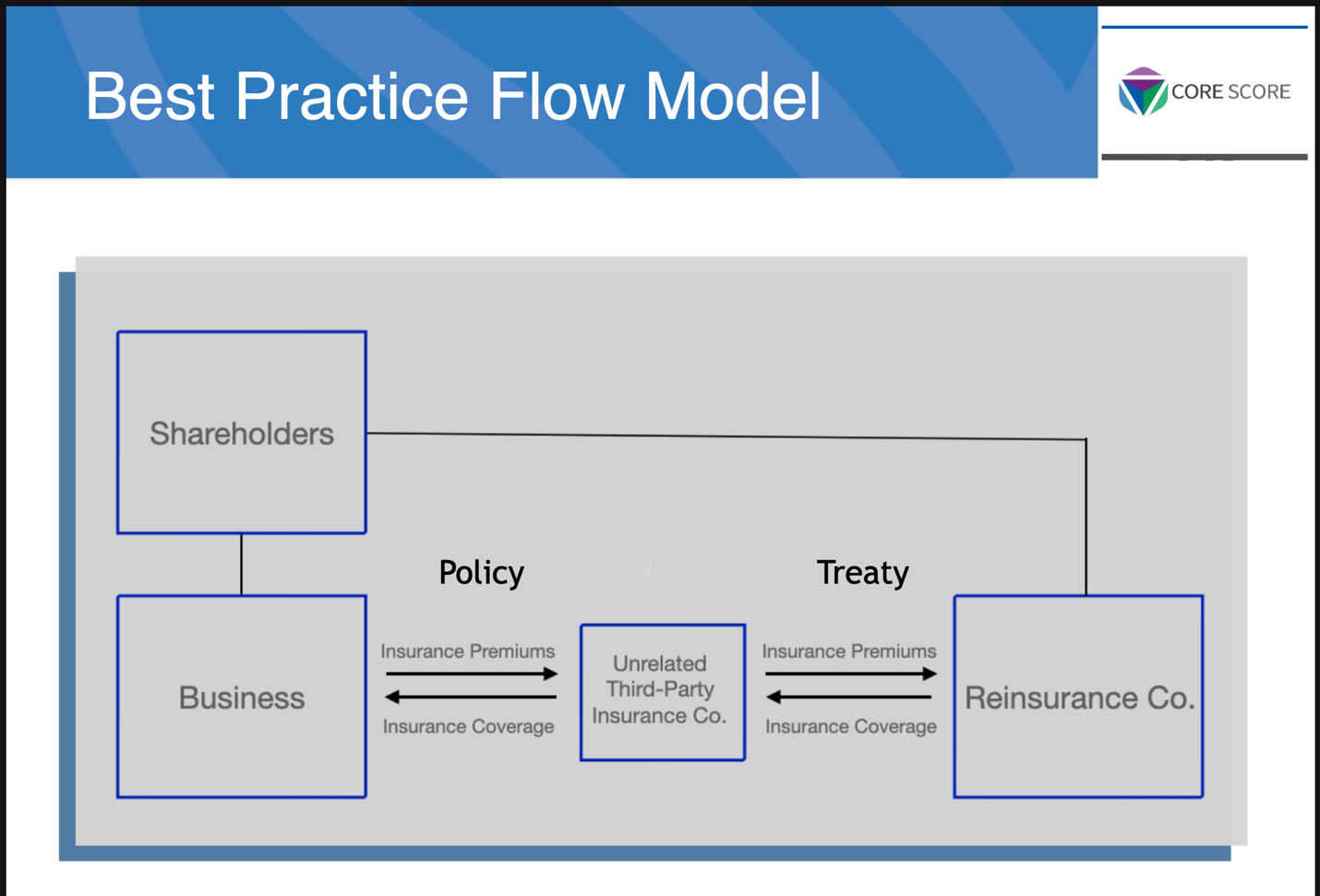

9. TRANSFER of RISK

At a glance, insurance (and therefore reinsurance) simply means ‘transfer of risk’.

Unlike a direct write structure (generally not recommended), be looking for a reinsurance model with two formal transfers of risk – one transaction by traditional insurance policy and the ensuing transaction by signed treaty. See the benefits of a POIC structure.

In a best practice POIC model, risk/premium is transferred from the business (insured) to the provider (insurance carrier); then after a time, this risk/premium is ‘laid off’ (reinsured) to another insurance entity. See representative image:

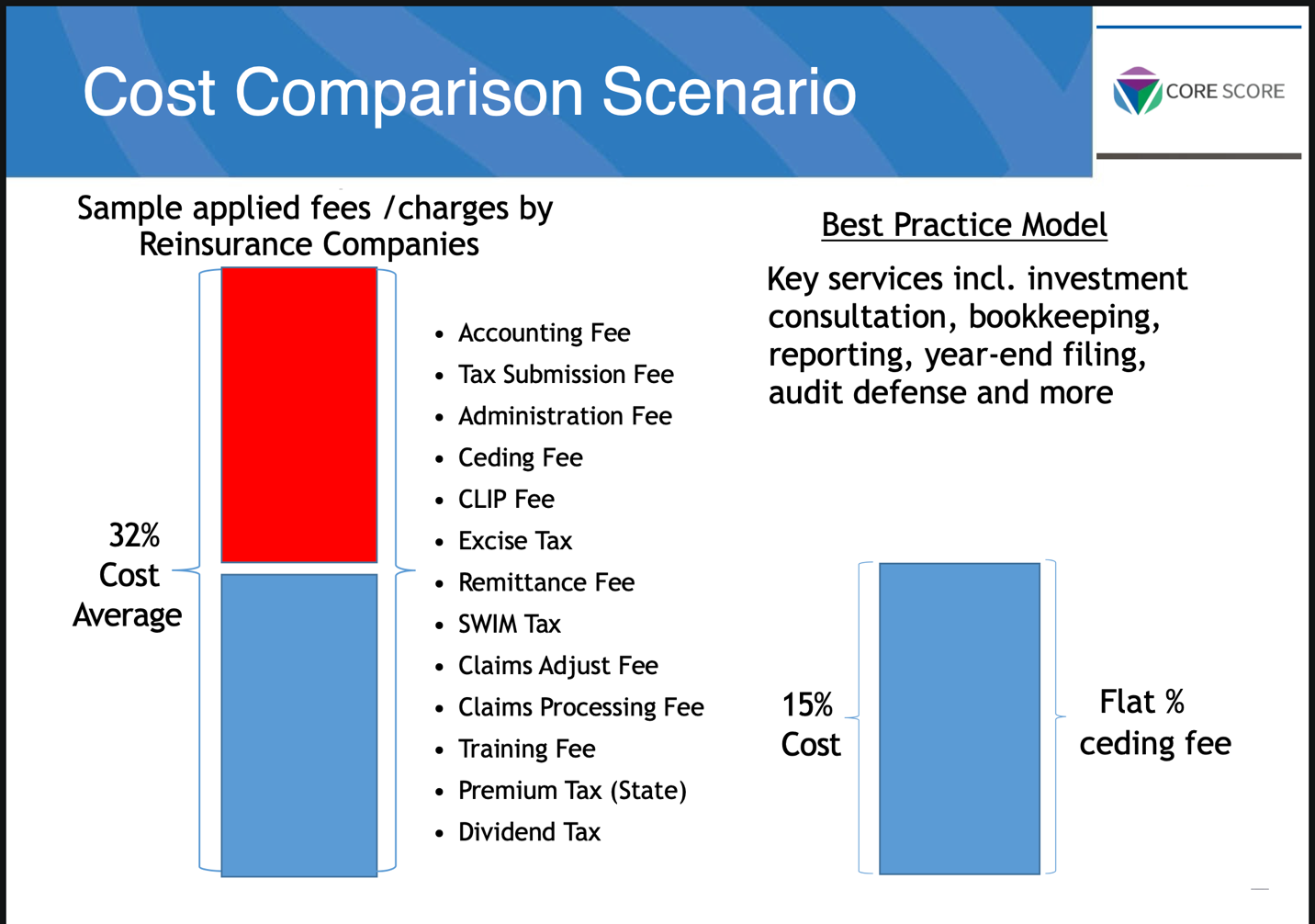

10. TRANSPARENT FEE STRUCTURE

Score Core suggests a reputational model which charges a modest capitalization fee (some providers charge $100,000 and more) and a modest ceding fee. It is important to understand if the ceding fee is a FLAT FEE, meaning this fee covers turnkey (wrap around) services from the provider with no hidden fees or extra charges.

Be skeptical of administrators/providers which charge ‘incidental fees’ including accounting fee, tax submission fee, admin fee, CLIP fee, excise tax, remittance fee, SWIM tax, claims adjust fee, claims processing fee, training fee, dividend tax and more. Avoid ‘extra costs’ including retained liability premium charged by the direct writer (additional fee tiered based on annual contributions). With this in mind, ask to see a sample cession statement from representative reinsurance providers.

Lastly, if the provider forces the business leader into using their specific financial institution, acknowledge that these institutions (having a holding plan of reserves) will also charge additional fees, charges and ‘taxes’.

See graphic representation:

Core Score’s Recommendation: The Latitude Plan™

A properly structured private insurance company gives you something the traditional market rarely does – control. Control over risk selection, claims timing, capital deployment and long-term wealth strategy.

By insuring uninsured and underinsured risk exposures through actuarially supported policies, you’re no longer just paying premiums – you’re repositioning them as a financial asset.

Across industries, Reinsurance Specialties™ clients adopt this best practice model – The Latitude Plan™ – to enhance risk management, mitigate losses, protect enterprise value and create a disciplined pathway for capital growth and generational wealth transfer.

Invitation

If your organization generates between $1M and $1B in annual revenue and is interested in learning more about private insurance and how The Latitude Plan™ may support your broader risk management strategy, we invite you to explore further.

You can review additional information here, or schedule an educational, no-obligation ZOOM call with the Core Score™ team or the Reinsurance Specialties™ team to determine whether this approach aligns with your business objectives.

Every private insurance platform works a little differently, and this information is for educational purposes only. As seasoned private insurance professionals, Reinsurance Specialties™ can provide more detail, share our best practice model and deliver consultative guidance for your specific needs.